.svg)

By Tim Attinger, President and Founder, OvationCXM

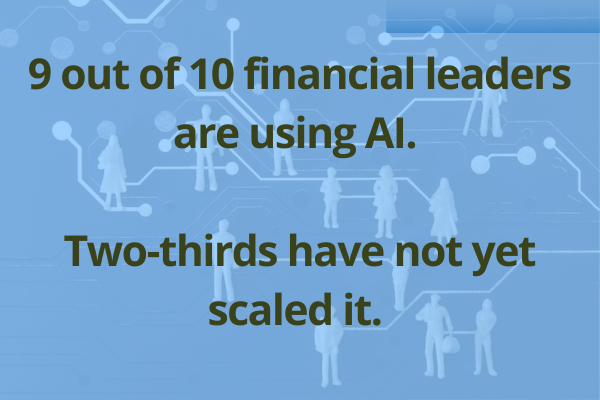

Nearly 9 out of 10 financial leaders say they're using AI, according to McKinsey & Company, but two-thirds have not yet scaled it. AI has proven its value; but financial institutions are finding it difficult to move past the pilot phase. For today, that's okay. But tomorrow? Missing out on opportunities to leverage AI will leave some banks behind. Orchestration has become necessary to enable a broader use of AI that delivers the ROI it promises.

Banks have perfected optimizing specific processes in specific functional areas to enhance efficiency. However, in commercial banking, these processes and the teams that manage them operate in isolation from one another, even though they fulfill a single product journey. Because of this fragmentation, execution is still a challenge.

At the same time, AI has introduced the opportunity to reimagine processes and service delivery, but these siloed operations limit that potential. Indeed, at the time of this writing, just 5% of AI initiatives are delivering ROI inside the banking industry.

TL;DR: AI Adoption is high. Operational maturity is not.

Most AI Is General-Purpose. Banking Execution Is Specific.

AI capabilities are increasingly accessible through either stand alone tools or embedded in point solutions. But they are typically built to deliver one main capability, regardless of industry or company. Banks, however, operate in highly specific workflows, passing work back and forth among segmented teams and partners to execute customer onboarding and servicing journeys.

These commercial banking workflows, embedded in business lines like merchant services, trade finance, treasury management and commercial cards, have strict mandates, leading to rigid sequences of tasks that must be performed in a specific order. At the same time, they are constantly juggling exceptions and personalization of journeys, due to unique customer segments, product type, geography, risk profile and ecosystem partners. While they must adhere to a standard procedure to meet regulatory compliance, they also have to balance catering to the needs and characteristics of each customer.

Categories of Banking CX Orchestration Complexity:

- Regulatory and Policy Requirements: Mandated steps and compliance checks

- Organizational Silos: Handoffs across multiple internal teams

- Technology Fragmentation: Legacy systems and isolated data environments

- Non-Standard Exceptions: Variations based on business type, risk, geography, and product

- External Dependencies: Critical steps owned by vendors, gateways and other third parties

That’s why a horizontal AI tool, even a good one, may produce limited value. It can speed up specific functions, providing summarizations or helping teams draft communication, but it cannot improve execution across a complete journey, to solve friction “in-between,” in the gaps and handoffs between different teams and platforms.

The bottleneck isn’t intelligence. It’s coordination.

.png)

Commercial Banking Scenario: Fine Until It Isn't

Here’s a common scenario. A commercial banking product onboarding is on track. SLAs are being met. Documentation is complete. Internal departments and vendor partners see no issues, and the client appears to be progressing in the journey.

However, the customer has actually become stalled at a step, but no one knows. Twenty-five percent of commercial banking customers have become so frustrated during onboarding that they’ve walked away before using the product they signed up for.

Business Banking CX Report

These journey failures, like most, didn’t happen within a single platform or team where it was obvious; they happened in the gap between platforms, departments and third parties, where status and responsibility become blurred. A customer’s interaction data lives in silos, rarely accessible to other teams or partners helping the customer.

Who owns the gap between steps? Who is responsible for issues if they fall between teams? How do teams and partners identify friction if they only see their part of the journey?

Coordination of onboarding or servicing has to be done in email threads, spreadsheets, and phone queues, which are not real-time, so teams operate in black holes, trying to support a customer with slivers of information. That’s why more than 50% of businesses report it takes multiple reach-outs to solve challenges with their commercial banking product.

This is also why standalone AI tools fall short. When they are deployed outside of an orchestrated journey, without context into ownership, sentiment, approvals or exceptions, they cannot reliably automate and optimize the full customer journey.

Operational Orchestration Is the Solution. AI Is the Enabler.

McKinsey’s research confirms what banks are learning in practice: scaling AI value requires integrating journey workflows, not isolated tasks.

This does not require ripping and replacing existing systems. Instead, it means deploying an orchestration layer to act as the central nervous system, connecting internal applications and ecosystem partners to eliminate communication and visibility gaps.

Orchestration is designed to unify CX operational information and make it visible for all stakeholders to act on, with context and ownership clearly defined.

Contextual Data Inside Orchestration

- Where the customer is in a process

- What steps are completed vs pending

- Who owns each step

- What approvals and policies apply

- What exceptions trigger a change in journey steps

- What communication is scheduled and when

At a high level, leadership gains insights into overall customer health, partner quality, business line efficiency and opportunities for revenue growth and cost savings across onboarding and servicing delivery.

AI Scaling Inside Contained Workflows

McKinsey notes that the transition from pilots to enterprise impact is still a work in progress for most organizations, even as its use expands dramatically. That’s especially relevant as agentic AI use cases gain momentum.

In McKinsey’s 2025 research, 23% of respondents report that their organizations are scaling an agentic AI system across the enterprise, and more have begun experimenting with agents.

In regulated environments, the right move is to exercise caution rather than push autonomy prematurely. AI should be deployed within defined workflows, and this is where an orchestration layer enforces containment.

AI within an orchestration layer is built with industry and institution-specific guardrails and parameters that govern its use:

- Clear permissions and policies

- Human-in-the-loop approvals, where needed

- Escalation paths for exceptions

- Auditability of actions and rationale

- Accountability for outcomes

This is where governed AI moves from a buzzword to essential infrastructure for banking modernization.

Where AI Creates Real Value First

When it comes to maximizing the value of AI, it is achieved most often in two main areas:

1) Execution support for internal teams

AI can create immediate operational value when embedded into orchestrated workflows:

- Summarizing the customer and case history immediately

- Surfacing product and policy guidance

- Recommending next-best actions within process and policy guidelines

- Drafting communication in a pre-set, approved brand voice

- Reducing manual follow-ups and status chasing

These high-frequency, labor-intensive activities directly slash a bank’s cost-to-serve and soften SLA pressure.

2) Customer-facing voice/chat with journey context

Voice and chat bots, when tied into full journey workflows:

- Can answer routine questions

- Route inquiries to the right owner

- Trigger a necessary next step

- Hand off customers with full context, vs a transcript

- Operate within determined policies and escalation rules

What Banking Leaders Should Do To Scale AI

For banking executives, the path to expanding AI judiciously across the organization to improve customer experience and operations includes three strategies:

1) Target Journeys With Execution Pain

Focus on journeys where delays create measurable pain:

- Time-to-revenue (commercial onboarding)

- Customer friction and churn risk (support/service)

- High exception volume

- Partner-heavy steps that create black boxes

Fix the journey flows that break most often and have the greatest impact on customer acquisition and retention.

2) Use AI Inside Operational Work Flows

The bank should not adapt its operating model to generic tools; AI should become embedded into the bank’s operating model, operating within its specific:

- Approvals and thresholds

- Role permissions

- Audit trails

- Escalation rules

- Guardrails for suggestions vs. actions

- Brand voice

3) Measure Execution Outcomes, Not Just AI Activity

Track the metrics that benefit operations and customer interactions:

- Journey duration

- Touches per case/per onboarding

- Time to resolution

- Exception rate and root causes

- Partner step aging and SLA adherence

- Cost-to-serve

- Escalation frequency

The Next Phase of AI in Banking

AI’s potential for transformation will be realized by how well financial institutions embed it into the daily workflows and customer journeys they manage today, bridging fragmented ecosystems and connecting third-party partners into cohesive operations.

That’s the only way AI will scale from isolated use cases in specific functional areas to broader use and expandion into human-in-the-loop automated workflows within banking functions.

The OvationCXM Perspective

OvationCXM recommends orchestration as a core operating system that coordinates onboarding and support journeys, connecting fragmented steps across operations, risk and partner ecosystems so AI can act on real-time context. This reduces onboarding delays, exception backlogs and manual coordination.

Leading industry analysts emphasize that AI ROI is driven by operating model redesign, accountability, and system integration. OvationCXM was architected specifically to provide this execution layer — embedding AI into governed, cross-team workflows rather than deploying it as another disconnected point solution.

The future of AI in banking CX operations will belong to institutions that integrate AI into their operational backbone to transform fragmented, ecosystem-wide onboarding and servicing processes into predictable, compliant customer journeys.

Learn about OvationCXM's orchestration operating system, built for the rigor of financial services.